If you already have a VA (Department of Veterans Affairs) home loan and rates have dropped since you bought, the VA IRRRL may be the simplest way to lower your monthly payment. IRRRL stands for Interest Rate Reduction Refinance Loan, and most people just call it the VA streamline refinance. It is designed to be fast and low-cost: less paperwork, a small funding fee, and in many cases no new appraisal and no income check. This guide explains how the VA IRRRL works, who qualifies, and how to tell whether refinancing is worth it.

What Is a VA IRRRL?

A VA IRRRL replaces your current VA loan with a new VA loan at a lower interest rate. It is called a streamline because the VA cut out much of the work required for a regular loan. You cannot use an IRRRL to pull cash out of your home or to refinance a non-VA loan; its one job is to lower the rate, and with it the monthly payment, on a loan you already have.

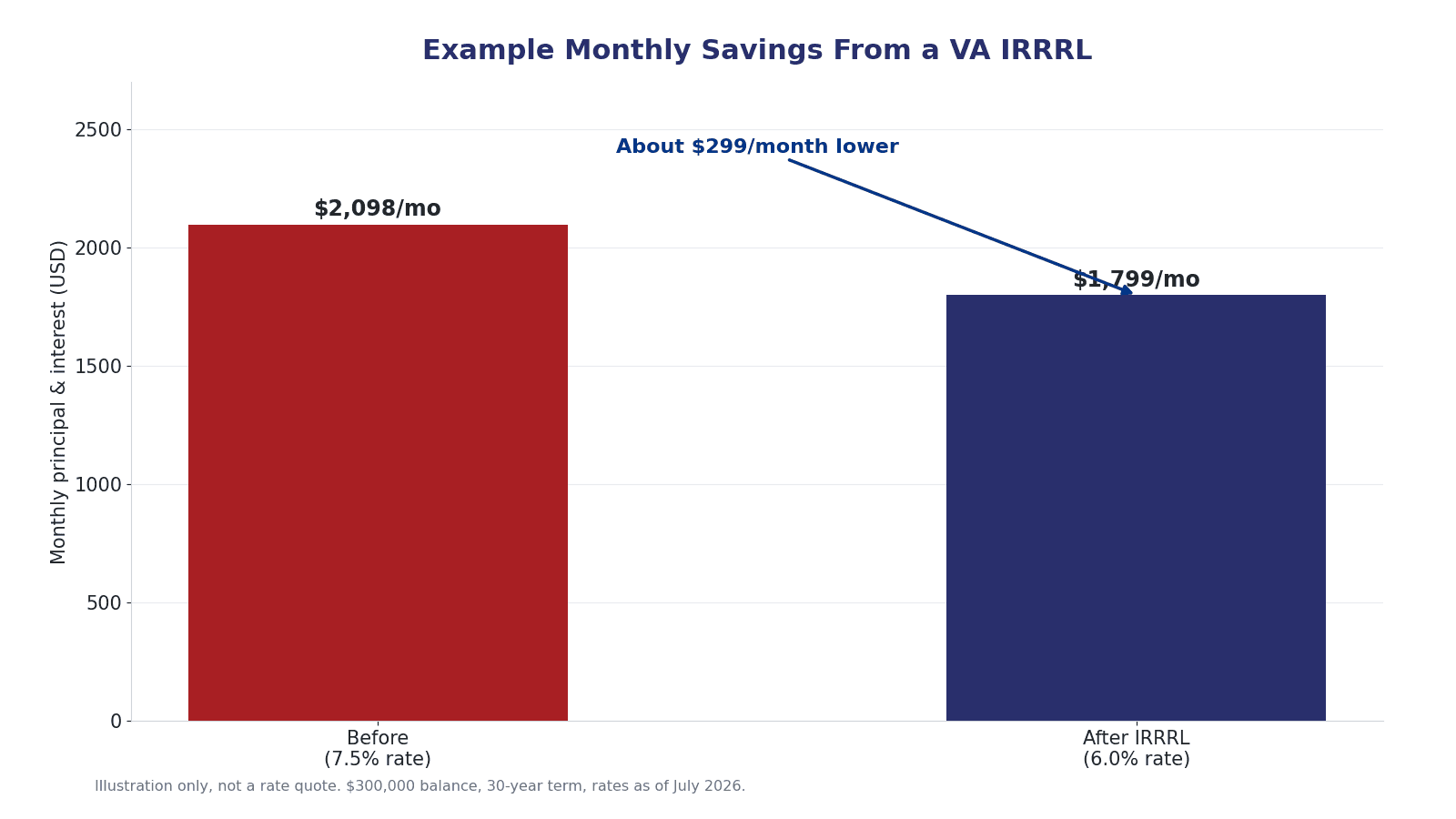

Because rates move over time, refinancing can make sense when they fall. As of July 9, 2026, Freddie Mac reported the average 30-year fixed mortgage rate at about 6.49 percent. If your current VA loan sits well above today's rates, an IRRRL is worth a look. For the bigger refinance picture, see should you buy now and refinance later.

How the VA IRRRL Is Different

Compared with your first VA purchase loan, the streamline skips several steps.

- Often no new appraisal is required, so you are not tied to a fresh home value.

- Income and employment verification are usually limited or waived.

- The VA funding fee is just 0.5 percent of the loan, far below a purchase loan's fee.

- You must already have a VA loan on the home; the IRRRL refinances that loan.

The low funding fee is a major reason the streamline is popular. According to VA.gov, the IRRRL funding fee is 0.5 percent, and it can be rolled into the new loan instead of paid in cash.

An illustration only, not a rate quote. Actual savings depend on your balance, rate, and term. Rates as of July 2026.

VA IRRRL Requirements

The VA and Congress added rules to make sure a streamline actually helps the veteran, not just the lender. The main ones are seasoning, net tangible benefit, and fee recoupment.

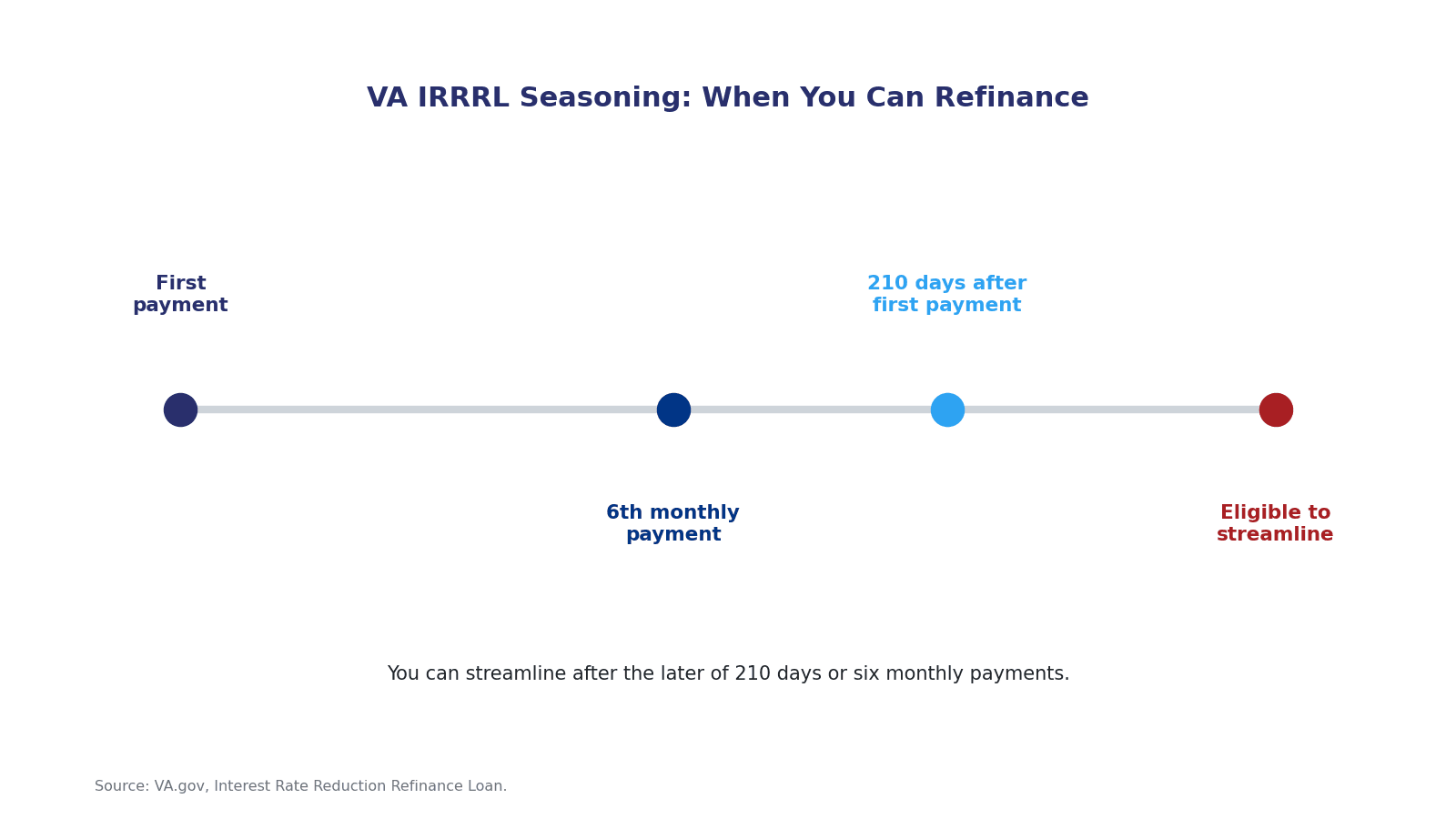

Seasoning: The 210-Day Rule

You cannot refinance the day after you close. Per the VA IRRRL page, your new loan cannot close until the later of two dates: 210 days after you made the first payment on your current loan, and the date you make your sixth monthly payment. In short, you generally need at least six on-time payments and about seven months of history before you can streamline.

Net Tangible Benefit

The refinance must leave you meaningfully better off, a standard the VA calls a net tangible benefit. Usually that means a lower interest rate, or moving from an adjustable rate to a fixed rate for stability. A lender cannot approve an IRRRL that does not clearly help you.