When you get PCS orders, one question comes up fast: how much house can I afford on BAH? Your BAH (Basic Allowance for Housing, the tax-free monthly amount the military pays you toward rent or a mortgage) is the natural starting point for a home budget, because it is money set aside for exactly this. This guide gives you a simple, four-step way to turn your allowance into a realistic home price, then explains the VA (Department of Veterans Affairs) loan rules that decide how much a lender will actually approve in 2026.

Start With Your BAH, Not a Guess

Civilians often use the "28 percent rule," which says housing should cost no more than 28 percent of your gross monthly income. For military families, there is a cleaner anchor: your BAH is already your housing budget. Because it is tax-free, a $2,100 allowance is worth more than $2,100 of taxable pay. That makes BAH a strong, honest baseline for what you can spend on a monthly payment.

Not sure what your rate is this year? Confirm it with the Department of Defense BAH rate lookup, and read our 2026 BAH rates explainer for what changed this year.

Four Steps to Turn BAH Into a Home Price

Here is the quick math. Every payment number below assumes a $0 down VA loan at about 6.6 percent, the conservative national average for a 30-year fixed VA purchase loan in early July 2026, per Bankrate's VA loan rates page. Rates vary by lender, and the VA does not set them.

- Start with your monthly BAH. That is your target payment ceiling.

- Subtract taxes and insurance. Set aside roughly $300 to $400 a month for property taxes and homeowner's insurance. What is left is your budget for principal and interest.

- Convert principal and interest into a loan amount. At about 6.6 percent, every $1,000 of loan costs roughly $6.39 a month. So divide your principal-and-interest budget by 6.39 and multiply by 1,000.

- That loan amount is close to your home price, because a VA loan needs $0 down.

For example, an E-6 with a $2,100 allowance might reserve $350 for taxes and insurance, leaving about $1,750 for principal and interest. Divide $1,750 by 6.39 and multiply by 1,000, and you get roughly a $274,000 loan, or about a $275,000 home with no money down.

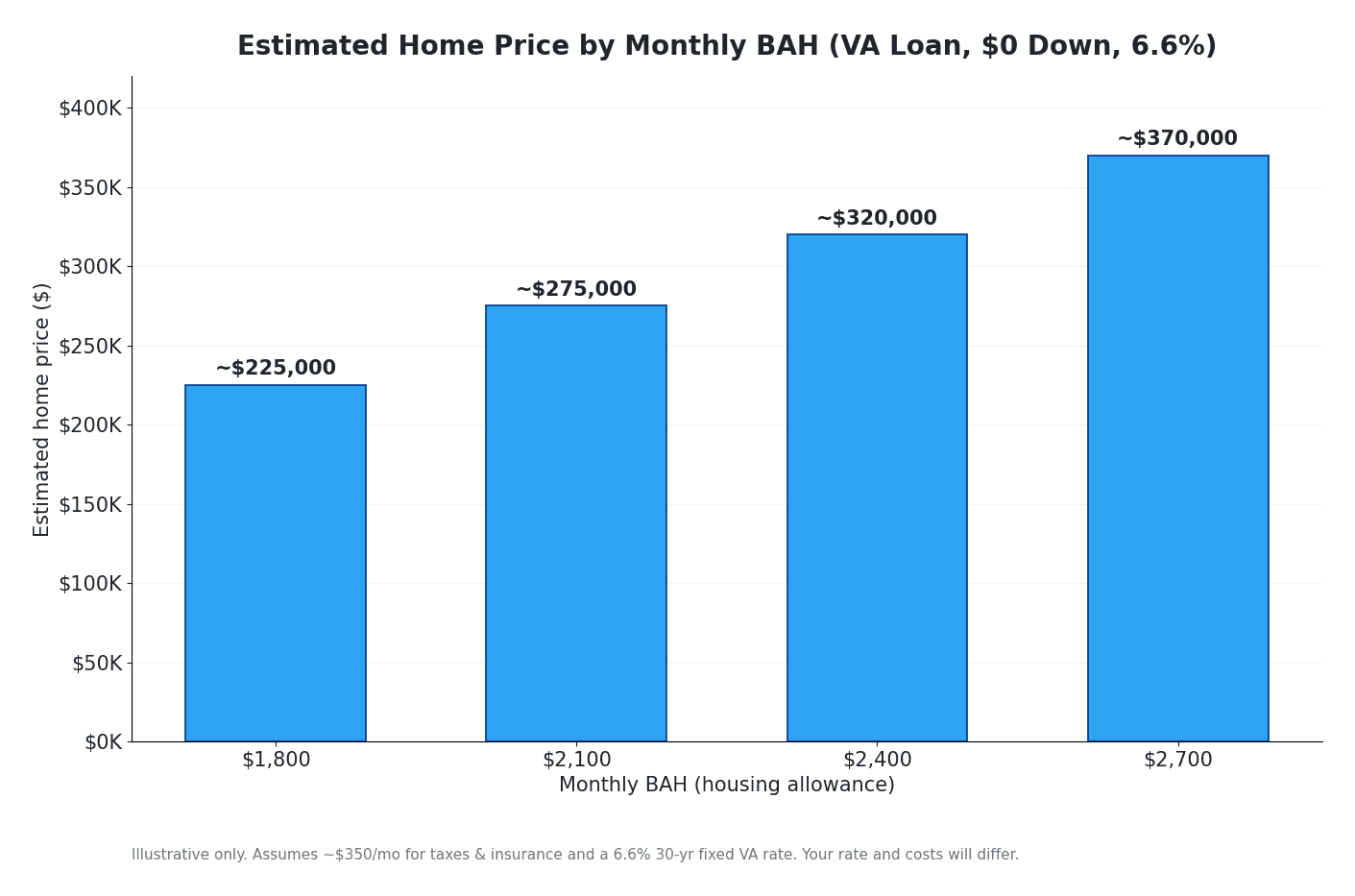

Estimated home price by BAH level at a 6.6 percent VA rate with $0 down and about $350 a month for taxes and insurance. Illustrative only; your rate and costs will differ.

The table below shows the same idea in numbers. Treat these as illustrations, not a quote.

| Monthly BAH | Left for principal & interest | Estimated home price ($0 down) |

|---|---|---|

| $1,800 | ~$1,450 | ~$225,000 |

| $2,100 | ~$1,750 | ~$275,000 |

| $2,400 | ~$2,050 | ~$320,000 |

| $2,700 | ~$2,350 | ~$370,000 |

Assumes a 6.6 percent VA rate, $0 down, and about $350 a month for taxes and insurance. A lower rate raises these numbers; a higher rate lowers them.

Why the VA Loan Stretches Your BAH

Two VA loan features make your allowance go further than it would with a conventional loan. First, eligible buyers put $0 down, so your BAH goes toward the loan instead of a down payment. Second, VA loans carry no private mortgage insurance, the extra monthly charge conventional lenders add when you put down less than 20 percent. Skipping it frees up more of your BAH for the actual loan. Our explainer on how a $0 down VA loan works walks through both benefits.