Before a lender can start your VA (Department of Veterans Affairs) home loan, they need proof you have earned the benefit. That proof is the VA loan Certificate of Eligibility, usually shortened to COE. It is a short document from the VA that confirms you meet the service requirements and shows how much loan guaranty, called entitlement, you have available. This guide explains what the COE is, the three ways to request one, and the papers to have ready so nothing slows your move.

What Is a VA Loan Certificate of Eligibility (COE)?

A VA loan Certificate of Eligibility is the VA's official confirmation that your military service qualifies you for the VA home loan program. It does two jobs. First, it verifies your service history meets VA rules. Second, it states your entitlement, which is the amount the VA will guarantee to your lender. That guaranty is what lets eligible buyers purchase with no down payment and no private mortgage insurance.

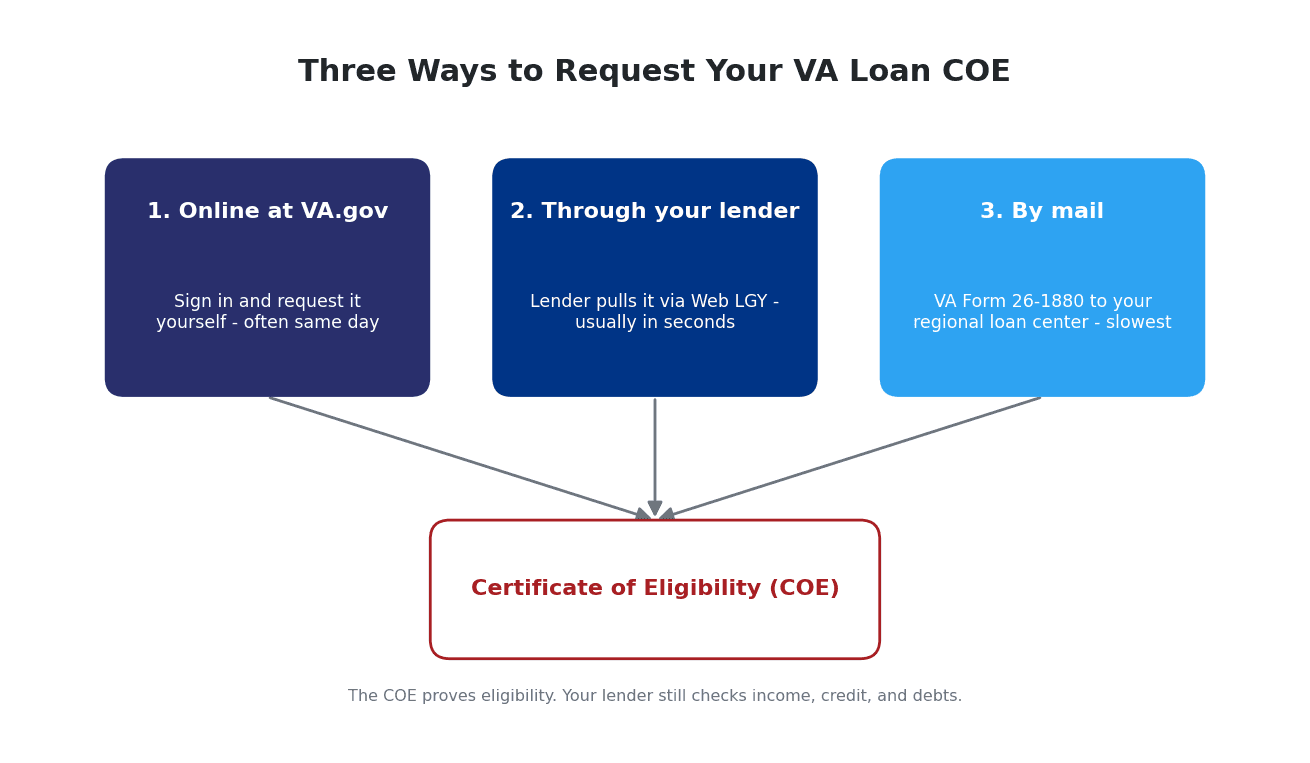

The COE is not a loan approval. It only proves eligibility. Your lender still checks your income, credit, and debts before approving the loan. Think of the COE as your ticket to the door; the lender decides what happens once you are inside.

For a wider look at how the benefit works, see our guide to the benefits of a VA loan and our explainer on how a $0 down VA loan works.

Do You Qualify? COE Eligibility at a Glance

You generally need a minimum amount of service to earn a COE. The exact requirement depends on when and how you served. The table below shows the common thresholds. Always confirm your situation against the official list, because service eras and duty types can change the rule.

| Who you are | Common service requirement |

|---|---|

| Active-duty service member | Currently serving, typically at least 90 continuous days |

| Wartime veteran | Roughly 90 continuous days of active service |

| Peacetime veteran | Roughly 181 continuous days of active service |

| National Guard or Reserve | About 6 years of service, or 90 days under a qualifying active-duty order |

| Surviving spouse | Spouse of a service member who died in the line of duty or from a service-connected condition, in many cases |

Source: VA.gov eligibility for VA home loan programs, which lists the full service requirements by era and duty type.

If you are not sure whether your record qualifies, our guide to VA loan eligibility requirements walks through the details in plain language.

Three Ways to Request Your COE

The VA gives you three paths to a COE. Most buyers use the first two because they are fast.

Request It Online Through VA.gov

You can sign in and request your COE yourself at VA.gov. Once you have a verified account, the request takes only a few minutes, and many members receive their certificate the same day. Start at the VA's how to request a COE page.

Ask Your Lender to Pull It

Most VA-experienced lenders can request your COE for you through the VA's Web LGY system. In many cases the system returns an approved certificate in seconds. This is often the easiest route because your lender is already gathering your documents. A VeteranPCS lender can handle this step as part of your pre-approval.

Mail VA Form 26-1880

If the online system cannot confirm your service, you can request the COE by mail. Fill out the Request for a Certificate of Eligibility, VA Form 26-1880, and mail it to your regional loan center at the address on the form. Mail requests take longer than the online or lender routes, so use this path only if the faster ones do not work.