Once your offer is accepted, the VA (Department of Veterans Affairs) loan appraisal is one of the biggest steps between you and your keys. A VA loan appraisal is an independent review that does two jobs at once: it estimates what the home is worth, and it checks that the property meets the VA's basic safety and livability rules. Understanding the VA loan appraisal helps you avoid surprises, especially when you are racing a report date. This guide explains what the appraiser looks for, how the appraisal differs from a home inspection, and what happens if the value comes in low or the home needs repairs.

What a VA Loan Appraisal Does

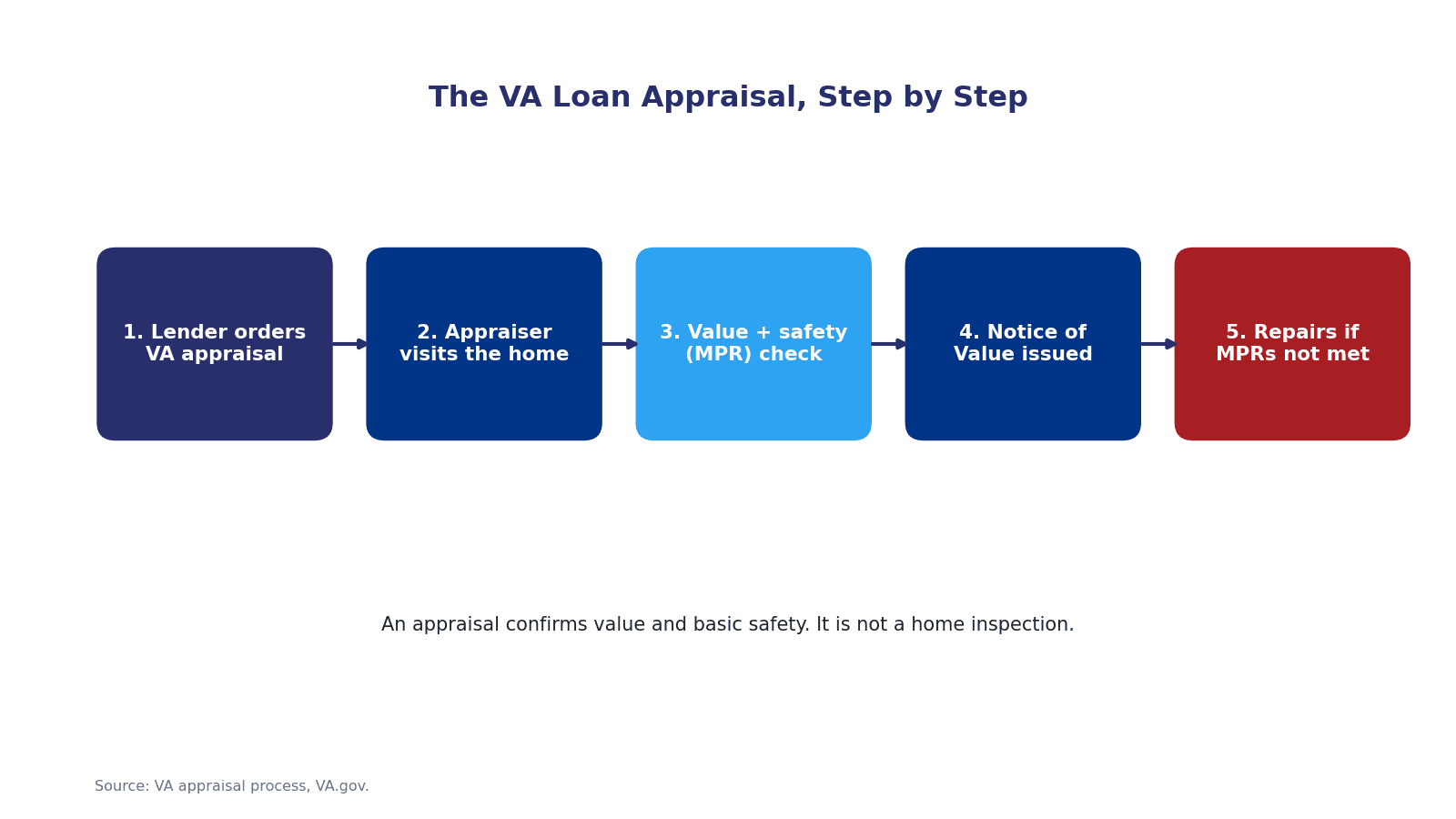

Every VA-backed purchase requires an appraisal ordered through the VA system and completed by a VA-assigned appraiser. The appraisal sets the maximum loan amount the VA will guarantee, and it confirms the home is safe, sound, and sanitary enough to be worth that loan.

The appraiser visits the property, measures it, photographs it, and compares it to recent nearby sales to reach an opinion of value. The final figure lands in a document called the Notice of Value, which your lender uses to finalize the loan. To keep your appraisal on schedule, have your Certificate of Eligibility and pre-approval ready before you go under contract.

VA Appraisal vs. Home Inspection

Buyers often mix these up, but they are not the same thing, and you usually want both.

| VA appraisal | Home inspection | |

|---|---|---|

| Who requires it | The VA and your lender | Optional, chosen by you |

| Main purpose | Confirm value and basic safety | Report the home's condition in detail |

| Who pays | Buyer (a seller can agree to cover it) | Buyer |

| Depth | A broad look at value and major issues | A close look at systems and defects |

The VA is clear on this point: an appraisal is not an inspection. As VA.gov explains, the appraiser is not an expert in the home's heating, cooling, plumbing, electrical, or roofing systems, and the VA guarantees the loan, not the condition of the house. If you want to know the true shape of the home before you buy, the VA recommends you hire a private inspector. It is money well spent before one of the biggest purchases of your life.

The VA appraisal moves through five basic steps. Source: VA appraisal process, VA.gov.

Minimum Property Requirements

The safety side of the appraisal is built around the VA's Minimum Property Requirements, or MPRs. These are the conditions a home must meet to protect your health and safety and to keep the property a sound investment. The VA's Minimum Property Requirement overview covers the full list, but common items include:

- Safe and reliable heating, water, and electrical systems

- A roof and structure in sound condition, with no major leaks

- No exposed wiring or obvious safety hazards

- Safe access to the home from a public or private street

- No standing water or drainage that threatens the foundation

If the appraiser sees something that does not appear to meet MPRs, VA rules say the appraiser recommends repairs, not a separate inspection. The item usually must be fixed before the loan can close. Many small repairs are handled by the seller as part of the deal, which is one more reason to work with an agent who knows VA transactions.

Ready to start your search with the appraisal in mind? Connect with a VeteranPCS lender to get pre-approved before you make an offer.